When we sit down with clients to discuss what they seek from their savings and investments it is not surprising that many are looking for certainty and peace of mind as well as a reasonable return. Going back 4-5 years ago the natural response was to take a trip down to the local high street bank, use a 1-2 year fixed rate deposit earning a net return of approximately 4% after basic rate tax.

However we are now in a period of low interest rates and persistent inflation, people are beginning to realise that the purchasing power of their savings is being eroded, yet they are struggling to identify better ways to balance their short-term and long-term financial priorities, and remain wary of investing.

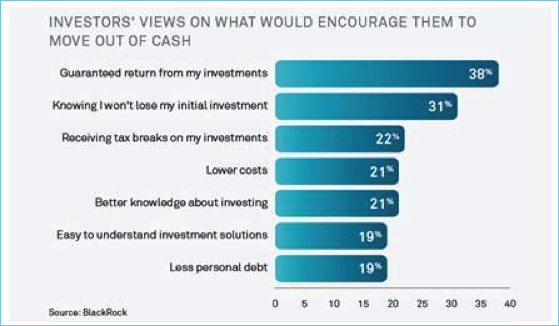

Following recent research (Source: Blackrock: ‘UK Investor Pulse Survey – What investors are thinking’) nearly half of investors intend to keep their allocation to cash at the same level over the next 12 months. And despite voicing concerns about whether they will be able to achieve longer-term goals, 32% of respondents plan to increase and 46% will retain their cash holdings.

Cash has come to represent a safety blanket in an uncertain world. Many people in the UK are choosing to sit on the sidelines of investing, having fallen into the habit of seeking shelter in cash and savings accounts. 68% of people’s investments are in cash, with a relatively small proportion dedicated to longer term investments, such as stocks and bonds.

People are very cautious in their overall approach to saving and investing. As a result of this cautious attitude, many people seem to be adopting a ‘wait and see’ attitude and are unwilling to make significant changes to their savings and investments over the next 12 months. This clearly shows that some people do not know what to do with their money and should be speaking to us.

The investment arena has developed considerably since the old days of with-profit endowment investments. As IFAs, we have good alternatives to cash for longer term investing which include guarantees applicable to the capital invested or guarantees to the income paid. Both of which are coupled with a cautious investment strategy and the ability to lock-in gains for the remainder of the investments life.

Could this be the security you need to move out of cash and make your savings work harder?

Elias Elia